“I Need to Save Money” then DON’T WASTE Your Money on (X) or You Can’t Afford (Y)

Don’t waste your money on what looks good today, but will mean nothing to you later.

Every day you say the same thing to yourself, “I need to save money,” and you finish each day staring at rising debt and a razor-thin bank account balance.

No money to buy the things you want and no way to invest in you or your loved ones’ futures.

How you got here may not entirely be your fault:

- Divorce

- Spousal abandonment

- Financial infidelity

- Poor financial choices

- Low income

- Maybe a combination of these

Either way, here you are and you want a way out.

All those items that you need or want, but can’t have, are a direct result of your misguided spending habits.

Today that changes.

Because today you will see the large amounts of money that go to waste on either your impulse purchases or your monthly expenses that you ignore.

[Take Poll]

Goals and Dreams: What Do You Really Want to Buy? And What Do You Need that You Currently Cannot Afford?

Want that Caribbean cruise with the kids or how about just fixing that annoying sound coming from your car’s engine that’s lasted for 2 months now? If that’s what you want then don’t waste your money on all that stupid stuff that you thought you wanted, but later didn’t end up using.

You wonder why you don’t have money to invest in your future? And you actually believe that you can’t afford that new laptop, but can you?

I think you can.

Because if I can go from $29,000 in debt to debt-free, to investing monthly in stocks and traveling 3-4 times a year, growing my emergency fund every week, buy a new computer, buy a new car on an average income then you can figure it out too.

In this post I will reveal ideas how to cut expenses, save money WITHOUT a second job nor any other ways to making extra money.

However, in a future post I will share relatively easy ways to make extra money that can help accelerate the speed in which you eliminate debt while simultaneously increasing savings.

You Chose to Put Yourself in Debt and to Lose Your Own Money

And Here’s How You Did It…

You see, it’s pretty simple.

Each week, each month you have a certain amount of money to spend.

For each person the amount is different.

And you purchase one thing, you sacrifice the opportunity to buy something else.

So, if you think about it, you make a trade, not so much a purchase.

Last week you took your family out to that steak house instead of preparing the chicken breast, tomato and mozzarella cheese salad and mixed grains with rice sitting in your fridge.

And if you had been tracking your expenses over the last 12 months you would see that you made a similar decision 25 other times.

Maybe not steak houses every time, but pizza, Mexican, seafood, etc.

As a result of this decision you removed, give or take, $75 each time away (about $25-30 for the cost of groceries for one dinner versus about $100 for steak dinner for a family of four including the tip) from your family cruise fund.

The total taken away from the cruise fund: $2,250.

AND THAT’S JUST FOR DINING OUT THOSE 25 TIMES!

We Love Impulse Buying

No, don’t misread that I said do not indulge on 10-ounce KC Ribeye with steak fries and an ice-cold beer, but you didn’t plan for those 25 meals out.

The sudden urge to go out to dinner hit you last second so you abandoned the plan to prepare dinner with the groceries you bought at the supermarket.

(And if you don’t prepare that meat sitting there soon, it will go bad, then that means you lost even more money towards your cruise).

If you had a budget to earmark money for dining out then it wouldn’t have affected your cruise money.

But now you’ve basically stolen from your vacation budget to pay for other urges.

It gets worse.

Wait until you see my entire list of places and ways you blow your money and further take away funds for that dream cruise.

Right now, in the next 3-5 minutes you will equip yourself with life-changing, financial fundamentals so that you don’t waste your money on more stupid stuff.

Learn how to keep money for what matters most to you.

Fixed vs. Variable Expenses: What We Spend their Hard-Earned Money On

The first step to plugging up that hole in your purse or wallet is to start tracking your expenses

And I suggest that you separate your expenses into two categories: fixed expenses and variable expenses.

What’s the difference? And why does it matter?

Fixed Expenses

Monthly costs that do not change such as rent, mortgage, health insurance, cable or satellite TV, Netflix, auto insurance, internet, car payment, cell phone bill (unless you purchase game apps or other extras), annual passes to theme parks, gym memberships, karate classes, dance lessons, etc.

Cutting or lowering fixed expenses can put a lot of money back in your pocket every month and over the course of the year.

Questions to Start Asking Yourself Regarding Fixed Expenses

How much extra does it cost for the premium cable packages? How often do you actually watch all those extra channels? In the eight months you’ve had that gym membership, how many times have you gone?

Can you eliminate or reduce any of your fixed expenses?

Variable Expenses

Monthly expenses that fluctuate. These are where the impulse purchases occur. All those Starbucks coffees, going to the movies, dining out, drinks at bars, new clothes, gasoline, sporting events, concerts, etc.

Properly managing your variable expenses can have the biggest impact on your ability to save more money because they make up the unnecessary expenses in your life.

However, variable expenses are the hardest to control because it takes strong self-discipline and a motivation-backed reason to not spend on one thing to save for another.

What do you want to save your towards?

A dream vacation?

How about a new car to replace the one that costs you a lot of money in repairs?

Do you want to save for something long-term like a house?

Or how about simply eliminating that big monkey on your back- credit card debt?

Without financial goals you have no reason to save and, therefore, no reasons to stop blowing your money on stupid things.

If your desire to finally take that trip to Ireland or Alaskan cruise were strong enough, then you’d start looking at all those coffee purchases differently.

You’d probably take a better look in your closet at the dozens of hangars and heap of clothes and accessories you’ve only worn once.

Questions to Start Asking Yourself Regarding Variable Expenses

Want that trip to Ireland?

How serious are you to eliminate that debt you’ve carried for years?

Don’t waste your money anymore on things that sound good when you buy them, but take away from the things that you really want in the long run.

How much do you spend on Starbucks annually?

What are your annual expenses for ALL the different sub-categories of variable expenses like clothing, gasoline, dining out on the run at fast food places, dining out at sit-down restaurants, entertainment, etc.?

Do you even know?

Why Tracking Expenses Will Change Your Life

When you categorize your expenses as either fixed and variable it gives you a crystal-clear view of how much money you spend each month.

You can calculate the fixed expenses more accurately then multiply by 12 to find your annual totals.

Looking at the variable expenses will make you sick because these are where the majority of the impulse purchases come from ($1,500 on coffee! OUCH!).

A budget, which sets the limits that you decide to spend on various categories of the variable expenses, will save you from slipping further into debt and not having money for the things that matter most.

Cruise or Coffee? Track Spending Habits, Cut Expenses Save Money

If you don’t have financial goals then this post then you have no reason to keep reading.

But let’s say that you do know what you want to save your for.

Then run a careful scan of both your fixed and variable expenses before you begin tracking them.

As you read over each item you purchase, start to ask yourself what you’d rather have, that item or your goal.

Next, jot down all of your expenses and then create categories on a spread sheet that match what you typically spend your money on.

Keep ALL receipts or just review your credit card/debit card statements from now on.

At least once a week fill in the totals for each category.

For example, if you went out twice for dinner in the first week of the month and the total came to $100 then place that amount under a category like “Dining Out- Sit Down Restaurants” for this month.

If later this month you spent $75 on dining out then add that to make the monthly “Dining Out- Sit Down Restaurants” total $175.

After a few months of reviewing all your expenses you will get a good idea where your money is going.

If you are like most people, then you will most likely feel disgusted with yourself on how much money you mismanage and waste.

Do you know what the average person spends their money on?

An article on Market Watch reveals what the typical American spends their money on.

If You Whine About Not Getting the Things You Want…Then Don’t Waste Your Money on These Items

How badly do you want to have money for your bigger purchases or to achieve your financial goals?

Then you must reconsider purchasing these items because you blow the majority of your money on this list of things.

I’ve divided the list between variable and fixed expenses.

Variable Expenses

- Dining Out Too Much (amounts that exceed your budget)

- Coffee, Soda, Junk Food

- Unnecessary Groceries

- Gasoline on Extra Mileage

- New Clothes You Rarely/Never Wear

- Brand Items

- Fun Nights Out

- Dress Shirts and Ties

- Shoes

- Duplicate/Excess Household and Grocery Items

- Overstock of Make-up

- Extra Laundry Loads

- Water Running…When NOT Using It

- Leaving Heating/Air Conditioning On When Not Home

- Name Brand Medicines

- Name Brand Groceries

- Premium Car Washes

What other items can you brainstorm that you purchase that sound good in the moment, but take away from the things you really want later?

Fixed Expenses

- Premium Cable Package

- High-Speed Internet

- Netflix Memberships

- Other Memberships or Subscriptions You Don’t Use

- Classes that You or the Kids No Longer Care About

- Bank Fees

- Annual Passes (and You Don’t Even Go)

- Credit Card Finance Fees and Credit Card Interest

- High Rent that Exceeds 30% of Total Living Expenses

- High Car Payments

- Poor Choice of Auto Insurance Coverage

- Expensive Cell Phone Data Plans

Have you jotted down all of your fixed expenses yet?

Did you review them and notice all the fixed expenses where you commit hard-earned money every month that could be used elsewhere?

If you haven’t done either of these things, then start, and don’t waste your money on monthly budget draining expenses anymore.

The Things You Need but Now Can’t Pay for Because You Wasted Your Money on Stuff You Don’t Use

Due to your mismanaged funds, you now cannot afford these items.

Some of the things on this list pop up during emergencies, and because you haven’t set up an emergency account, you plunge deeper in credit card debt.

Other items below, you want, but won’t ever get until you take control of your spending habits.

- Oil Changes

- Investments: 401k, 529 Plan, Mutual Funds, Stocks

- Pay Off Credit Card Debt Faster

- Flights/Vacations

- Preventative Car Maintenance

- Tires

- Laptop

- Cell Phone

- Work Clothes/Shoes

- Pet Expenses

- Real Estate License

- Start New Business/ Launch New Blog

- AAA Membership (to pay for 100-mile emergency tows)

- Car Registration

- Contacts/Glasses

Don’t Waste Your Money Anymore!

Are You Ready to Take the First Step?

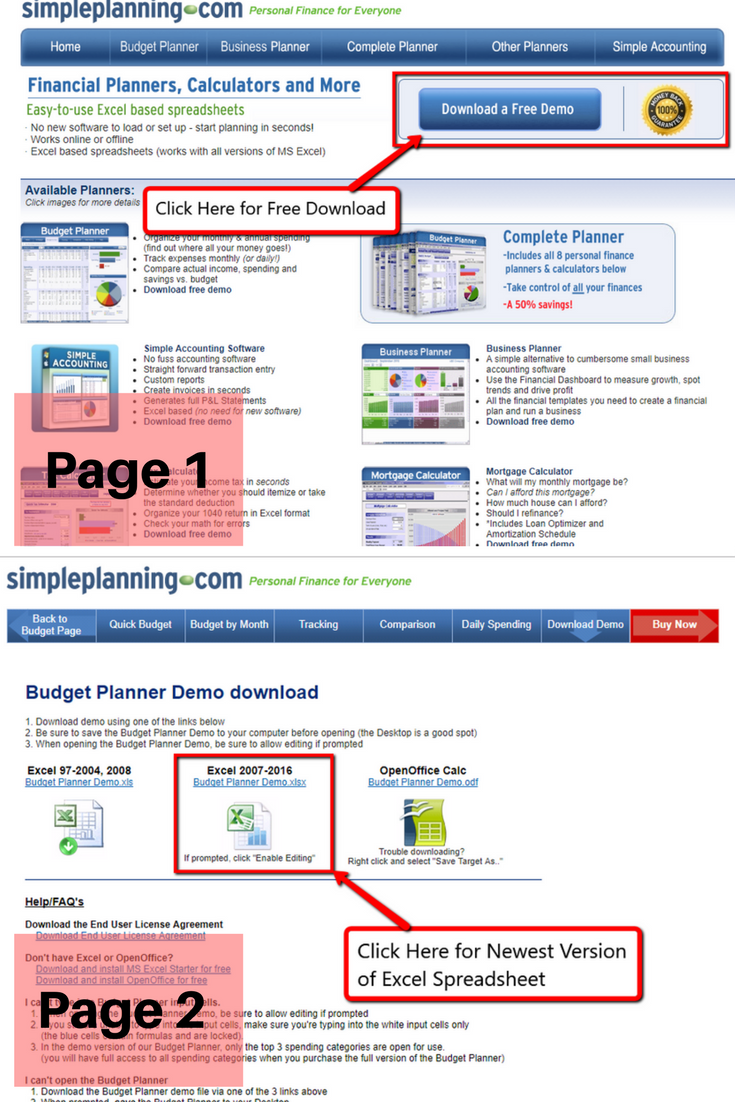

Download this Free, Simple Household Expense Spreadsheet

[Click Here] to download free household spreadsheet demo.

This spreadsheet is pretty detailed and covers multiple expense and savings categories.

For $15.95 you can purchase your own copy of it.

It may take a little while to completely get used to, but it is more thorough than the free one above.

In fact, watch a free video demonstration of how to use it.

[Click Here] to get a free sample of the detailed household expense spreadsheet.

Don’t waste your money or another minute on missing out on your financial goals.

Take action today!

Other Related Posts

Selling House During Divorce: “Should I Sell My House Quick or Wait?”